June 13, 2018

Validity Team

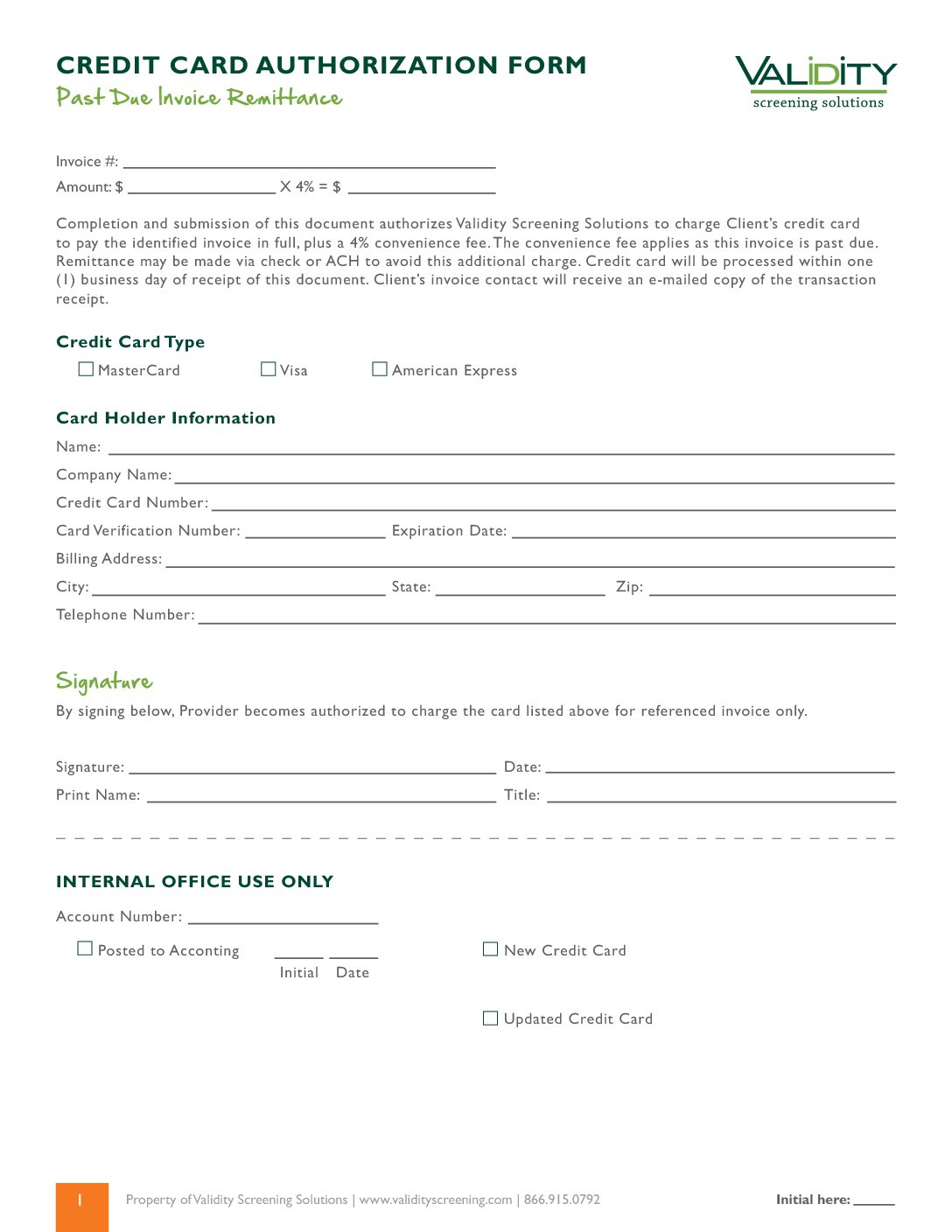

Estimated Read Time: 5 Minutes<http:///iframe></p> <ul style="list-style-type: disc;"> <li>The Fair Credit Reporting Act governs the use of background checks in the employment process and requires a sufficient Disclosure and Authorization form<http:///li> <li>Litigation around the Disclosure and Authorization has been on the rise and continues to be the most heavily litigated subject of employment screening<http:///li> <li>The language used in a Disclosure and Authorization form should be clear, concise, and to-the-point in order to help applicants understand the process<http:///li> <li>Make sure to separate your Disclosure and Authorization forms from your job application<http:///li> <li>Separating the Disclosure from the Authorization is not required by the FTC but we do suggest you take this action to help protect from potential litigation in the future<http:///li><http:///ul><span id="more-6711"></span><br /> <hr> <p><span style="font-size: 1.6rem; background-color: transparent;"> <img decoding="async" src="https:http:///http:///validityscreen.wpengine.comhttp:///wp-contenthttp:///uploadshttp:///BG-Check-Disclosure_website-2.png" alt="Background Check Disclosure and Authorization" width="1920" style="width: 1920px;"><http:///span><http:///p></p> <p>The Fair Credit Reporting Act (FCRA) governs the use of all consumer reports. Since background checks are classified as “consumer reports” under the FCRA, it’s important to ensure that you’re following the letter of the law to the “T.” With the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) both having a hand in the regulation of the FCRA, there’s no shortage of regulation to go around. But by far, the heaviest litigated piece of the FCRA is the need for a Disclosure and Authorization form.<http:///p></p> <p>So that got me thinking, “If the Disclosure and Authorization forms are so essential to compliance, what are some keys to look out for when drafting your own?”<http:///p></p> <p>Well, back in April of 2017, the FTC released information on how employers can best use their Disclosure and Authorization forms and still remain in compliance with the Fair Credit Reporting Act. While the article they wrote doesn’t contain a whole lot of information specific to what you can include in your Disclosure and Authorization, it did contain a few golden nuggets that highlight what the FTC looks for when examining compliant Disclosure and Authorization documents.<http:///p></p> <p> <http:///p></p> <h2>What Can’t You Include?<http:///h2></p> <p>If you examine what the FTC stated in April of 2017, it becomes clear that the FTC doesn’t point out many things that you SHOULD include in your Disclosure and Authorization, but they do include a hefty list of things that you SHOULD NOT include.<http:///p></p> <p>Here’s the list that we’ve come up with based upon what the FTC has said:<http:///p></p> <ul> <li>Do not include legal jargon. All statements made in the Disclosure and Authorization should be intelligible to your average prospective employee.<http:///li> <li>Do not include any wording that purports to require the prospective employee to acknowledge that your hiring decisions are based on legitimate, non-discriminatory reasons.<http:///li> <li>Do not include extraneous acknowledgments or waivers – including claims to release you from liability for conducting, obtaining, or using the background screening report.<http:///li> <li>Do not include overly broad authorizations that permit the release of information that the FCRA does not allow to be included in a background screening report.<http:///li> <li>Do not include a certification by the prospective employee that all information in his or her job application is accurate.<http:///li> <li>Do not use small fonts or illegible type that makes the Disclosure and Authorization difficult to read.<http:///li><http:///ul> <p> <http:///p></p> <table style="border-color: #f47820; border-style: solid;"> <tbody> <tr> <td> <table> <tbody> <tr> <td style="padding: 20px; width: 35%;"><a href="https:http:///http:///offers.validityscreening.comhttp:///the-companion-guide-to-compliant-background-screening-practices" rel="noopener noreferrer" target="_blank"><img decoding="async" src="https:http:///http:///validityscreen.wpengine.comhttp:///wp-contenthttp:///uploadshttp:///Background-screening-eBook-1-2.png"><http:///a><http:///td></p> <td style="padding: 20px 20px 20px 40px; width: 55%;"><strong style="background-color: transparent; font-size: 1.6rem; color: #4b4b4b;">Compliant Background Screening Practices<http:///strong> <br />The Companion Guide</p> <p style="line-height: 1;"><span style="font-size: 12px;">The topic of Background Checks is a tricky labyrinth to navigate these days. Let us help with the directions.<http:///span><http:///p></p> <p style="line-height: 1;"><span style="font-size: 12px;"><a href="https:http:///http:///offers.validityscreening.comhttp:///the-companion-guide-to-compliant-background-screening-practices" target="_blank" rel="noopener noreferrer"><img decoding="async" src="https:http:///http:///no-cache.hubspot.comhttp:///ctahttp:///defaulthttp:///2061251http:///98906c64-cf2e-448f-8c4c-cd5286fbf4f6.png"><http:///a><http:///span><http:///p><http:///td><http:///tr><http:///tbody><http:///table><http:///td><http:///tr><http:///tbody><http:///table></p> <p> <http:///p></p> <p> <http:///p></p> <p>You’ll notice a common theme with most of these items – the FTC wants to ensure that your prospective employees understand what it is that they’re signing and what their rights are as the subject of a consumer report. They do not want you to include “extra stuff” because it makes it harder for the prospective employee to understand the main purpose of the Disclosure and Authorization. The FTC claims that it may even violate the FCRA.<http:///p></p> <p>The bottom line is, the FTC wants you to be clear, succinct, and to-the-point to add clarity for all prospective employees and job candidates that will be signing off on these Disclosure and Authorization forms. Including any extraneous information, fluffy non-descript information, overly broad terms, or anything that works to dilute the message of the Disclosure and Authorization forms could be seen as additional information that is not needed. To summarize the FTC’s entire stance in one simple statement, “keep it simple.”<http:///p></p> <p>If it isn’t essential to the message of your Disclosure and Authorization, don’t include it.<http:///p></p> <p>If you feel that you need to include other documents, such as a Release of Liability, the FTC recommends that you place those additional disclosures in a separate document – not attached to the Disclosure and Authorization whatsoever.<http:///p></p> <p> <http:///p></p> <h2>What Should You Include?<http:///h2></p> <p>After looking at the FTC’s guidance on what not to include, you may be wondering if you should simply send a blank piece of paper as to <a href="https:http:///http:///blog.validityscreening.comhttp:///10-common-background-check-disclosure-authorization-form-mistakes">avoid any violations of the FCRA<http:///a>. In keeping with the theme of simplicity, you walk a fine line between being descriptive and convoluting the message. We’ve put together a solid list of items that need to be included in your Disclosure and Authorization forms to ensure that your prospective employees have a clear and thorough understanding of what it is they’re signing.<http:///p></p> <ul> <li>You must include clear and concise language that describes the need for and use of the background check.<http:///li> <li>You must define the scope of the background check to include the specific criteria that you will be screening (e.g. driving records, sex offender registry, credit report, etc.).<http:///li> <li>You must include the contact information of the Consumer Reporting Agency on the Disclosure and Authorization in the event that your prospective employee has a dispute of the information within their consumer report.<http:///li> <li>You must include language that references the Summary of Rights document as a separate document.<http:///li><http:///ul><br /> <h2>Standalone Disclosure and Authorization<http:///h2></p> <p>It is important that you ensure your Disclosure and Authorization are separate from your application. High profile litigation has resulted from numerous organizations displaying their Disclosure and Authorization directly on the job application. If you currently display your Disclosure and Authorization in this way, it is critical that you remove it from your job applications.<http:///p></p> <p>While the Disclosure and Authorization must be standalone and separate from any other documentation, the FTC has stated that they do not require that the Disclosure and Authorization forms be separate from each other. However, we have established a best practice of separating the Disclosure and Authorization forms from each other based upon the increase in litigation that we’ve seen alleging that employers willfully violate the FCRA by obtaining consumer reports on the basis of legally invalid authorization forms that contained additional disclosures and information.<http:///p></p> <p> <http:///p></p> <h2>Wrapping Up<http:///h2></p> <p>With so many nuances and possibilities for technical violations of the FCRA within your Disclosure and Authorization forms, it’s important to stay on top of the ever-changing landscape of employment screening. While much of the screening world’s attention is on “Ban the Box” at the moment, Disclosure and Authorization forms still account for the vast majority of all litigation in employment screening.<http:///p></p> <p>We’d love to know what you think or answer any questions you may have. Please leave a comment below to tell us your thoughts. For more great blogs and content please subscribe to our blogs <a href="http:///" rel="noopener noreferrer" target="_blank">here<http:///a>.<http:///p></p> </section></div> </div> </div> <div id="mc_embed_signup" class="newsletter"> <div class="newsletter-container"> <p>Join 24,000+ Email Subscribers</p> <form action="//validityscreening.us8.list-manage.com/subscribe/post?u=28352954dbb82978c91f85fef&id=c5096bdb5d" method="post" id="mc-embedded-subscribe-form" name="mc-embedded-subscribe-form" class="validate" target="_blank" novalidate> <div class="mc-field-group"> <input type="text" placeholder="First" value="" name="FNAME" class="required" id="mce-FNAME"> </div> <div class="mc-field-group"> <input type="text" placeholder="Last" value="" name="LNAME" class="required" id="mce-LNAME"> </div> <div class="mc-field-group"> <input type="email" placeholder="E-mail" value="" name="EMAIL" class="required email" id="mce-EMAIL"> </div> <input type="hidden" name="b_28352954dbb82978c91f85fef_c5096bdb5d" tabindex="-1" value=""> <input type="submit" value="»" name="subscribe" id="mc-embedded-subscribe" class="btn"> <div class="response" id="mce-error-response" style="display:none"></div> <div class="response" id="mce-success-response" style="display:none"></div> </form> </div> </div> <script type='text/javascript' src='//s3.amazonaws.com/downloads.mailchimp.com/js/mc-validate.js'></script><script type='text/javascript'>(function($) {window.fnames = new Array(); window.ftypes = new Array();fnames[4]='FNAME';ftypes[4]='text';fnames[0]='EMAIL';ftypes[0]='email';fnames[2]='LNAME';ftypes[2]='text';fnames[3]='CNAME';ftypes[3]='text';fnames[8]='ROLE';ftypes[8]='text';fnames[5]='INDUSTRY';ftypes[5]='text';fnames[7]='SOLUTIONS';ftypes[7]='text';fnames[6]='CITY';ftypes[6]='text';fnames[1]='STATE';ftypes[1]='text';fnames[9]='AE';ftypes[9]='text';fnames[10]='ADATE';ftypes[10]='date';fnames[11]='IDATE';ftypes[11]='date';fnames[12]='LEADM';ftypes[12]='text';fnames[13]='LEADS';ftypes[13]='text';fnames[14]='SOLINT';ftypes[14]='dropdown';}(jQuery));var $mcj = jQuery.noConflict(true);</script> <!--End mc_embed_signup--> <div class="footer"> <div class="footer-container"> <div class="widgets"> <div class="widget-area"> <div id="nav_menu-2" class="widget widget_nav_menu"><div class="menu-footer-left-container"><ul id="menu-footer-left" class="menu"><li id="menu-item-835" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-has-children menu-item-835"><a href="https://validityscreening.com/about-us/">About Us</a> <ul class="sub-menu"> <li id="menu-item-836" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-836"><a href="https://validityscreening.com/about-us/our-story/">Our Story</a></li> <li id="menu-item-837" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-837"><a href="https://validityscreening.com/about-us/meet-the-team/">Meet the Team</a></li> <li id="menu-item-834" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-834"><a href="https://validityscreening.com/about-us/our-partners/">Our Partners</a></li> <li id="menu-item-838" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-838"><a href="https://validityscreening.com/about-us/community-engagement/">Community Engagement</a></li> </ul> </li> <li id="menu-item-839" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-has-children menu-item-839"><a href="https://validityscreening.com/screening-solutions/">Screening Solutions</a> <ul class="sub-menu"> <li id="menu-item-841" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-841"><a href="https://validityscreening.com/?page_id=77">For Employers</a></li> <li id="menu-item-840" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-840"><a href="https://validityscreening.com/for-educators-ret/">For Educators</a></li> <li id="menu-item-842" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-842"><a href="https://validityscreening.com/?page_id=81">For Volunteer Coordinators</a></li> <li id="menu-item-4885" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-4885"><a href="https://validityscreening.com/screening-solutions/for-athletic-directors/">For Athletic Directors</a></li> <li id="menu-item-843" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-843"><a href="https://validityscreening.com/screening-solutions/all-solutions/">All Solutions</a></li> </ul> </li> </ul></div></div> </div> <div class="widget-area"> <div id="nav_menu-4" class="widget widget_nav_menu"><div class="menu-footer-middle-container"><ul id="menu-footer-middle" class="menu"><li id="menu-item-821" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-821"><a href="https://validityscreening.com/technology/">Technology</a></li> <li id="menu-item-820" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-has-children menu-item-820"><a href="https://validityscreening.com/resources/">Resources</a> <ul class="sub-menu"> <li id="menu-item-923" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-923"><a href="https://validityscreening.com/resources/compliance/">Compliance</a></li> <li id="menu-item-950" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-950"><a href="https://validityscreening.com/?page_id=946">Webinar Series</a></li> <li id="menu-item-4519" class="menu-item menu-item-type-custom menu-item-object-custom menu-item-4519"><a href="https://validityscreening.com/videos/">ValidityTV</a></li> </ul> </li> <li id="menu-item-2915" class="menu-item menu-item-type-custom menu-item-object-custom menu-item-2915"><a href="http://blog.validityscreening.com">Blog</a></li> </ul></div></div> </div> <div class="widget-area"> <div id="nav_menu-3" class="widget widget_nav_menu"><div class="menu-footer-right-container"><ul id="menu-footer-right" class="menu"><li id="menu-item-7050" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-7050"><a href="https://validityscreening.com/contact/">Contact Us</a></li> <li id="menu-item-2075" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-2075"><a href="https://validityscreening.com/privacy-policy/">Privacy Policy</a></li> <li id="menu-item-7550" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-7550"><a href="https://validityscreening.com/accessibility-statement/">Accessibility Statement</a></li> <li id="menu-item-4971" class="menu-item menu-item-type-post_type menu-item-object-page menu-item-4971"><a href="https://validityscreening.com/background-check-policy/"><br/><br/><br/>Building a Background Check Policy</a></li> </ul></div></div> </div> <div class="widget-area"> <a class="btn" href="/schedule-demo">Contact Us »</a><br><div class="search-box">X</div> <form method="get" class="animated fadeInDown" id="searchform" action="https://validityscreening.com/"> <input type="text" size="put_a_size_here" name="s" id="s" value="Search the site..." onfocus="if(this.value==this.defaultValue)this.value='';" onblur="if(this.value=='')this.value=this.defaultValue;"/> </form> </div> </div> <div class="footer_info_container"><img src="https://validityscreening.com/wp-content/uploads/2015/09/footerlogo.png" style="float: none"><img src="https://validityscreening.com/wp-content/uploads/2019/11/Accreditation_Logo_Transparent_FINAL.png" style="width:20%; float: none; margin-left: 10%"><br><br><p style="color: #ffffff;">© <script type="text/javascript"> document.write(new Date().getFullYear()); </script> Validity Screening Solutions</p></div> <div class="social_media"> <a href="https://twitter.com/ValidityScreen" class="smlink" target="_blank"><i class="fa-stack fa-2x"><i class="fa fa-circle fa-stack-2x"></i><i class="fa fa-twitter fa-stack-1x"></i></i></a> <a href="https://www.linkedin.com/company/validity-screening-solutions" class="smlink" target="_blank"><i class="fa-stack fa-2x"><i class="fa fa-circle fa-stack-2x"></i><i class="fa fa-linkedin fa-stack-1x"></i></i></a> <a href="https://www.youtube.com/channel/UCFznIovAGhVMRhcuR755dYQ" class="smlink" target="_blank"><i class="fa-stack fa-2x"><i class="fa fa-circle fa-stack-2x"></i><i class="fa fa-youtube fa-stack-1x"></i></i></a> <a href="https://www.facebook.com/ValidityScreening/" class="smlink" target="_blank"><i class="fa-stack fa-2x"><i class="fa fa-circle fa-stack-2x"></i><i class="fa fa-facebook fa-stack-1x"></i></i></a> <!-- <a href="https://www.instagram.com/validityscreen/" class="smlink" target="_blank"><i class="fa-stack fa-2x"><i class="fa fa-circle fa-stack-2x"></i><i class="fa fa-instagram fa-stack-1x"></i></i></a> --> <!-- Removed Instagram --> </div> </div> </div> <script type="text/javascript">jQuery(document).ready(function(){var PostId = "6711";var SubmittedURL = "https://validityscreening.com/blog/blogs/what-to-include-on-a-background-check-disclosure/";jQuery("input[name=SpokalPostId]").each(function(){this.value = PostId;});jQuery("input[name=SpokalSubmittedUrl]").each(function(){if(!this.value){this.value = SubmittedURL;}});jQuery("input[name=SpokalRedirectUrl]").each(function(){if(!this.value){this.value = SubmittedURL;}});});</script> <script type="text/javascript">jQuery(".gform_body").append('<input id="SpokalPiwikId" name="SpokalPiwikId" type="hidden">');</script> <script type="text/javascript">var globalPiwikId;function spokalSavePiwikId(piwikID){globalPiwikId = piwikID;jQuery(".spokalPiwikID").val(piwikID);jQuery("input[name=SpokalPiwikId]").val(piwikID);}</script> <script type="text/javascript"> function sp_set_cv(){ _paq.push(['setCustomVariable',3,'SP_POST_ID','6711','page']); } </script> <script>if ( typeof window.twttr == 'undefined' ) {window.twttr = (function(d, s, id) {var js, fjs = d.getElementsByTagName(s)[0],t = window.twttr || {};if (d.getElementById(id)) return t;js = d.createElement(s);js.id = id;js.src = 'https://platform.twitter.com/widgets.js';fjs.parentNode.insertBefore(js, fjs);t._e = [];t.ready = function(f) {t._e.push(f);};return t;}(document, 'script', 'twitter-wjs'));}</script><link rel='stylesheet' id='tf-footer-style-css' href='https://validityscreening.com/wp-content/plugins/tf-numbers-number-counter-animaton/inc/tf-footer-style.css?ver=1000' type='text/css' media='all' /> <script type="text/javascript" id="theme-my-login-js-extra"> /* <![CDATA[ */ var themeMyLogin = {"action":"","errors":[]}; /* ]]> */ </script> <script type="text/javascript" src="https://validityscreening.com/wp-content/plugins/theme-my-login/assets/scripts/theme-my-login.min.js?ver=7.1.7" id="theme-my-login-js"></script> <script type="text/javascript" src="https://validityscreening.com/wp-content/themes/validity/colorbox-master/jquery.colorbox-min.js?ver=1.6.3" id="colorboxjs-js"></script> <script type="text/javascript" src="https://validityscreening.com/wp-content/plugins/pardot/js/asyncdc.min.js?ver=7c7757011653c25b411eab1447a4251c" id="pddc-js"></script> <script>'undefined'=== typeof _trfq || (window._trfq = []);'undefined'=== typeof _trfd && (window._trfd=[]),_trfd.push({'tccl.baseHost':'secureserver.net'}),_trfd.push({'ap':'wpaas'},{'server':'01032ebe-2414-1571-445e-84e883984b5d.secureserver.net'},{'pod':'A2NLWPPOD08'},{'storage':'a2cephmah003pod08_data06'},{'xid':'41213427'},{'wp':'6.5.2'},{'php':'8.0.30'},{'loggedin':'0'},{'cdn':'1'},{'builder':''},{'theme':'validity'},{'wds':'0'},{'wp_alloptions_count':'643'},{'wp_alloptions_bytes':'319025'})</script> <script>window.addEventListener('click', function (elem) { var _elem$target, _elem$target$dataset, _window, _window$_trfq; return (elem === null || elem === void 0 ? void 0 : (_elem$target = elem.target) === null || _elem$target === void 0 ? void 0 : (_elem$target$dataset = _elem$target.dataset) === null || _elem$target$dataset === void 0 ? void 0 : _elem$target$dataset.eid) && ((_window = window) === null || _window === void 0 ? void 0 : (_window$_trfq = _window._trfq) === null || _window$_trfq === void 0 ? void 0 : _window$_trfq.push(["cmdLogEvent", "click", elem.target.dataset.eid]));});</script> <script src='https://img1.wsimg.com/tcc/tcc_l.combined.1.0.6.min.js'></script> <script src='https://img1.wsimg.com/traffic-assets/js/tccl-tti.min.js' onload="window.tti.calculateTTI()"></script> </div> <script type="text/javascript"> _linkedin_partner_id = "157930"; window._linkedin_data_partner_ids = window._linkedin_data_partner_ids || []; window._linkedin_data_partner_ids.push(_linkedin_partner_id); </script><script type="text/javascript"> (function(){var s = document.getElementsByTagName("script")[0]; var b = document.createElement("script"); b.type = "text/javascript";b.async = true; b.src = "https://snap.licdn.com/li.lms-analytics/insight.min.js"; s.parentNode.insertBefore(b, s);})(); </script> <noscript> <img height="1" width="1" style="display:none;" alt="" src="https://dc.ads.linkedin.com/collect/?pid=157930&fmt=gif" /> </noscript> </body> </html>